The banking industry’s digital transformation imperative has reached a critical inflection point. While fintech competitors deploy new capabilities in weeks, traditional financial institutions struggle with mainframe systems processing billions in daily transactions through COBOL applications that predate the internet.

The strategic challenge isn’t replacing these battle-tested systems—it’s unlocking their data and business logic for modern digital banking experiences. Leading financial institutions are implementing five distinct modernization patterns that preserve regulatory compliance and operational reliability while enabling real-time customer experiences and competitive digital products.

- Pattern 1: Customer Experience APIs – Digital Banking Enablement

- Pattern 2: Real-Time Risk Management – Fraud Prevention and Compliance

- Pattern 3: Open Banking API Architecture – Platform Business Models

- Pattern 4: Core Banking Modernization – Service-Oriented Architecture

- Pattern 5: Data-Driven Banking – Analytics and AI Enablement

- Banking-Specific Implementation Considerations

- Strategic Investment Planning for Banking Modernization

- Banking Industry Success Factors

- Measuring Banking Modernization Success

- Strategic Implications for Banking Technology Leadership

Pattern 1: Customer Experience APIs – Digital Banking Enablement

The Customer Experience API pattern transforms traditional banking mainframes into real-time service platforms supporting mobile banking, online portals, and omnichannel customer experiences.

Strategic Business Value

Banks implementing customer experience APIs achieve 250-400% increases in mobile banking adoption within 12 months. Customer acquisition costs decrease 30-40% when account opening processes reduce from days to minutes. Customer satisfaction scores improve 20-35% with real-time balance updates and transaction processing.

Core Banking Integration Requirements

Modern digital banking requires real-time access to fundamental banking services:

- Account Management: Balance inquiries, transaction history, account status updates

- Payment Processing: Wire transfers, ACH transactions, bill pay services

- Credit Operations: Application processing, limit adjustments, payment posting

- Customer Onboarding: KYC verification, account creation, product enrollment

- Fraud Detection: Real-time transaction monitoring and alert generation

Regulatory Compliance Considerations

Banking APIs must maintain SOX compliance, PCI DSS certification, and regulatory audit trails. Implementation requires:

- End-to-End Encryption: TLS 1.3 minimum for all customer data transmission

- Authentication Integration: Seamless connection with existing bank security systems (RACF, ACF2)

- Audit Logging: Complete transaction trails linking API calls to core banking records

- Data Sovereignty: Ensuring customer data remains within regulatory jurisdictions

Implementation Success Metrics

Regional banks report 60-80% reduction in digital product launch timelines. Customer onboarding automation increases from 20% to 85% within 18 months. Mobile banking transaction volumes typically grow 300-500% as real-time capabilities replace next-day batch processing.

Investment Framework

Customer experience API implementations require 4-8 month development cycles with $1M-$3M initial investment. ROI materializes within 12-18 months through:

- Customer acquisition cost reduction: $200-$500 per new customer

- Operational efficiency gains: 40-60% reduction in customer service volume

- Revenue growth: $5M-$15M annually from improved digital banking adoption

Pattern 2: Real-Time Risk Management – Fraud Prevention and Compliance

The Real-Time Risk Management pattern enables instant fraud detection, regulatory reporting, and risk analytics using live mainframe transaction data streams.

Financial Risk Mitigation Value

Banks implementing real-time risk management reduce fraud losses by 35-60% through instant transaction analysis. Regulatory reporting accuracy improves 90%+ while preparation time decreases from weeks to hours. Credit risk assessment becomes dynamic instead of periodic, enabling $10M-$50M additional lending capacity through better risk quantification.

Technical Architecture Requirements

Real-time risk platforms require sophisticated data streaming and analysis capabilities:

- Transaction Stream Processing: Sub-second analysis of all payment transactions

- Historical Pattern Analysis: Machine learning models trained on decades of transaction history

- Regulatory Data Marts: Real-time population of Basel III, CCAR, and Dodd-Frank reporting systems

- Alert Management: Instant notification systems for suspicious activity and compliance violations

Fraud Detection Enhancement

Modern fraud detection requires analyzing transaction patterns impossible with batch processing:

- Velocity Checking: Real-time monitoring of transaction frequency and amounts

- Geographic Analysis: Location-based risk assessment for card and digital transactions

- Behavioral Modeling: Machine learning detection of unusual customer behavior patterns

- Network Analysis: Cross-customer transaction pattern recognition

Regulatory Reporting Modernization

Real-time compliance reporting transforms regulatory burden into competitive advantage:

- Stress Testing: Dynamic capital adequacy calculations using live portfolio data

- Liquidity Management: Real-time LCR and NSFR calculations for optimal funding decisions

- Credit Risk Monitoring: Continuous PD, LGD, and EAD calculations for loan portfolios

- Market Risk Assessment: Live VAR calculations incorporating latest market data

Business Impact Quantification

Community banks implementing real-time risk management report:

- Fraud detection accuracy: 85% improvement in true positive rates

- False positive reduction: 60% decrease in legitimate transaction blocks

- Regulatory examination scores: Significant improvement in risk management ratings

- Lending efficiency: 25-40% faster credit decision processing

Pattern 3: Open Banking API Architecture – Platform Business Models

The Open Banking API Architecture pattern transforms banks from product providers into platform businesses, enabling fintech partnerships and embedded financial services.

Strategic Platform Value

Banks implementing open banking architectures capture 15-25% of fintech revenue through partnership models. API monetization generates $2M-$10M annually for mid-size institutions. Customer retention improves 20-30% through expanded service ecosystems.

PSD2 and Regulatory Compliance

Open banking implementations must satisfy regulatory requirements while enabling business growth:

- Strong Customer Authentication: Multi-factor authentication for all API access

- Consent Management: Granular customer control over data sharing permissions

- Data Standardization: ISO 20022 messaging and OpenAPI 3.0 specifications

- Third Party Provider Management: Certification and monitoring of API consumers

API Product Strategy

Successful open banking platforms offer tiered API products:

- Account Information APIs: Balance and transaction data for PFM applications

- Payment Initiation APIs: Third-party payment processing capabilities

- Identity Verification APIs: KYC and identity services for fintech partners

- Credit Decision APIs: Real-time creditworthiness assessment for lending platforms

- Fraud Prevention APIs: Risk scoring services for e-commerce and marketplace platforms

Revenue Model Innovation

Open banking enables multiple revenue streams:

- Transaction Fees: Per-API-call pricing for payment processing services

- Data Licensing: Anonymized transaction data for market research and analytics

- White-Label Banking: Core banking services for fintech and corporate clients

- Embedded Finance: Banking services integrated into non-financial applications

Partnership Ecosystem Development

Leading banks report 50+ fintech partnerships within 24 months of open banking launch. Partnership revenue typically represents 10-20% of digital banking income. Customer acquisition through partnerships costs 60-80% less than traditional marketing channels.

Pattern 4: Core Banking Modernization – Service-Oriented Architecture

The Core Banking Modernization pattern transforms monolithic banking applications into service-oriented architectures while preserving transaction integrity and regulatory compliance.

Business Agility Enhancement

Banks implementing service-oriented core systems achieve 50-70% faster product development cycles. New financial products launch in weeks instead of months. Cross-selling effectiveness improves 40-60% through real-time customer insight access.

Service Decomposition Strategy

Modern core banking architectures decompose traditional systems into focused services:

- Customer Management Service: Centralized customer data and relationship management

- Account Management Service: Deposit, loan, and investment account operations

- Transaction Processing Service: Payment, transfer, and settlement operations

- Product Catalog Service: Banking product definitions and pricing rules

- Interest Calculation Service: Complex interest and fee calculation engines

- Regulatory Reporting Service: Compliance data aggregation and reporting

Transaction Integrity Preservation

Banking service architectures require sophisticated consistency management:

- Saga Patterns: Distributed transaction coordination without compromising availability

- Event Sourcing: Complete audit trails for all account and transaction changes

- ACID Compliance: Transaction atomicity preservation across service boundaries

- Eventual Consistency: Balanced consistency models for non-critical data synchronization

Legacy Integration Approach

Service modernization follows risk-managed phases:

- API Exposure: Existing mainframe functions become accessible services (6 months)

- Critical Path Modernization: High-volume transaction services move to modern platforms (12 months)

- Customer-Facing Modernization: Services supporting digital channels get priority treatment (18 months)

- Regulatory Service Updates: Compliance and reporting services modernize incrementally (24 months)

Technology Investment Requirements

Core banking modernization requires substantial investment:

- Development Teams: 15-25 FTE including mainframe and cloud-native expertise

- Infrastructure: Cloud-native platforms with mainframe connectivity

- Timeline: 24-36 month comprehensive transformation

- Budget: $10M-$50M depending on institution size and complexity

Pattern 5: Data-Driven Banking – Analytics and AI Enablement

The Data-Driven Banking pattern makes decades of banking transaction history accessible to modern analytics, machine learning, and artificial intelligence platforms.

Customer Intelligence Value Creation

Banks implementing comprehensive data analytics achieve:

- Customer lifetime value prediction accuracy: 70-85% improvement

- Cross-selling conversion rates: 200-300% increase through targeted offers

- Customer churn prediction: 6-month early warning with 80%+ accuracy

- Personalized pricing: 15-25% revenue increase through dynamic rate optimization

Modern banking analytics require comprehensive data accessibility:

- Customer 360 Views: Complete relationship history including all products and interactions

- Transaction Behavior Analysis: Spending pattern recognition and prediction

- Credit Risk Modeling: Real-time assessment using complete payment history

- Market Risk Analytics: Portfolio optimization using historical performance data

- Operational Risk Detection: Process anomaly identification and efficiency optimization

Machine Learning Applications

Banking AI initiatives demonstrate measurable business impact:

- Credit Underwriting: Automated loan decisions for 80-90% of applications

- Fraud Detection: Real-time transaction scoring with 95%+ accuracy

- Customer Service: Chatbot resolution rates exceeding 70% for routine inquiries

- Investment Advisory: Robo-advisor platforms managing $100M+ in assets

- Regulatory Compliance: Automated suspicious activity report generation

Data Architecture Requirements

Banking analytics platforms require sophisticated data management:

- Real-Time Streaming: Transaction data available for analysis within seconds

- Historical Data Lake: Complete banking history accessible for machine learning training

- Data Governance: Customer privacy protection and regulatory compliance automation

- Self-Service Analytics: Business user access to banking data through governed interfaces

Competitive Advantage Metrics

Data-driven banks report significant performance improvements:

- New product development: 60% faster through customer insight integration

- Risk-adjusted returns: 20-30% improvement through better pricing and risk assessment

- Operational efficiency: 40% cost reduction through process automation and optimization

- Customer satisfaction: 25-35% improvement through personalized banking experiences

Banking-Specific Implementation Considerations

Financial services modernization requires specialized expertise in banking regulations, risk management, and operational continuity.

Regulatory Compliance Framework

Banking modernization must satisfy comprehensive regulatory requirements:

- Federal Reserve Guidance: SR 11-7 on model risk management and IT governance

- OCC Standards: Cloud computing and vendor management requirements

- FDIC Expectations: Operational resilience and business continuity planning

- State Banking Regulations: Varying requirements across banking charter jurisdictions

Risk Management Integration

Banking systems require enterprise risk management integration:

- Operational Risk: Technology change management and business continuity planning

- Credit Risk: Loan portfolio monitoring and regulatory capital calculation

- Market Risk: Trading book management and interest rate risk assessment

- Liquidity Risk: Cash flow monitoring and funding requirement optimization

Business Continuity Requirements

Banking modernization cannot compromise operational availability:

- 99.99% Uptime: Core banking systems require extreme reliability

- Disaster Recovery: Cross-region failover capabilities with RPO/RTO under 1 hour

- Regulatory Reporting: Uninterrupted compliance reporting during system transitions

- Customer Service: Zero disruption to customer-facing banking services

Examination Readiness

Modernized banking systems must satisfy regulatory examination requirements:

- Model Validation: Machine learning and AI model governance and testing

- Data Quality: Comprehensive data lineage and quality monitoring

- Vendor Management: Third-party risk assessment for cloud and technology providers

- Cybersecurity: Enhanced security controls for distributed banking architectures

Strategic Investment Planning for Banking Modernization

Banking technology leaders must develop comprehensive modernization roadmaps that balance innovation with risk management.

Phase 1: Digital Banking Foundation (6-12 months, $2M-$5M)

Objectives: Enable competitive digital banking capabilities Scope: Customer experience APIs for mobile and online banking Success Metrics: 300%+ mobile adoption growth, 50% customer service cost reduction Risk Mitigation: Parallel operation with existing systems, comprehensive rollback capabilities

Phase 2: Real-Time Risk and Compliance (12-18 months, $3M-$8M)

Objectives: Modernize risk management and regulatory reporting Scope: Real-time fraud detection, compliance automation, regulatory data marts Success Metrics: 50% fraud loss reduction, 90% regulatory reporting automation Business Value: Enhanced examination ratings, improved capital efficiency

Phase 3: Open Banking Platform (18-24 months, $5M-$12M)

Objectives: Create platform revenue streams and fintech partnerships Scope: Open banking APIs, partner onboarding, revenue sharing models Success Metrics: $5M+ partnership revenue, 50+ fintech integrations Strategic Value: Market expansion beyond traditional banking boundaries

Phase 4: Core Banking Transformation (24-48 months, $15M-$50M)

Objectives: Achieve industry-leading operational efficiency and product agility Scope: Service-oriented core banking, complete system modernization Success Metrics: 70% faster product development, 40% operational cost reduction Long-term Impact: Sustainable competitive advantage in digital banking

Banking Industry Success Factors

Successful banking modernization requires specialized organizational capabilities and strategic focus.

Executive Leadership Requirements

Board-Level Technology Understanding: Banking boards must comprehend technology strategy importance for competitive positioning Chief Digital Officer Roles: Dedicated executive leadership for digital transformation initiatives Risk Committee Oversight: Technology risk integration with traditional banking risk management Regulatory Relationship Management: Proactive regulator engagement on modernization initiatives

Specialized Skills Development

Banking Technology Expertise: Teams combining mainframe knowledge with cloud-native capabilities Regulatory Technology Specialists: Professionals understanding both banking regulations and modern technology architectures Data Scientists: Advanced analytics professionals with banking domain knowledge Cybersecurity Professionals: Enhanced security expertise for distributed banking architectures

Strategic Partnership Management

Technology Vendor Relationships: Strategic partnerships with banking technology specialists Consulting Expertise: External expertise for specialized modernization challenges Regulatory Advisory: Legal and compliance advisory for technology transformation Industry Collaboration: Participation in banking technology consortiums and standards bodies

Measuring Banking Modernization Success

Banking modernization success requires measurement across financial performance, operational efficiency, and strategic positioning dimensions.

Financial Performance Indicators

- ROE Enhancement: 15-25% improvement through operational efficiency and revenue growth

- Cost-to-Income Ratio: 20-30% improvement through automation and process optimization

- Revenue Per Customer: 40-60% increase through cross-selling and product innovation

- Customer Acquisition Cost: 50-70% reduction through digital channels and partnerships

Operational Excellence Metrics

- System Availability: Maintained or improved 99.99% uptime during modernization

- Transaction Processing Speed: Real-time capabilities replacing batch processing delays

- Regulatory Compliance: 100% automated compliance reporting for applicable regulations

- Customer Service Efficiency: 60-80% reduction in routine inquiry resolution time

Strategic Positioning Measures

- Digital Banking Market Share: Competitive positioning in mobile and online banking

- Fintech Partnership Revenue: Platform business model success through API monetization

- Innovation Velocity: Time-to-market for new banking products and services

- Regulatory Leadership: Recognition as technology innovation leader by banking regulators

Strategic Implications for Banking Technology Leadership

Banking modernization represents the most significant technology transformation in financial services since the introduction of electronic banking. Success requires understanding that modernization enables strategic business model evolution, not just operational improvement.

The five patterns provide proven frameworks for banking transformation while maintaining the reliability, security, and regulatory compliance that define successful financial institutions. Banks implementing these patterns systematically achieve sustainable competitive advantages through superior customer experiences, operational efficiency, and platform business models.

Banking technology leaders who master these modernization patterns position their institutions for sustained success in the digital financial services landscape. The strategic imperative is clear: transform proven banking systems into modern platform capabilities that enable new business models while preserving the trust and reliability that customers expect from financial institutions.

Executive banking leadership requires implementing these patterns not as technology projects, but as strategic business transformation initiatives that unlock the full potential of decades of banking expertise and customer relationships.

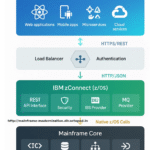

A modern banking digital experience illustration: mobile banking app screen connected to a legacy mainframe through an API gateway, glowing data streams showing real-time account updates. Include icons for account management, payments, and KYC. Background: sleek corporate blue gradient with circuit patterns. Style: clean, infographic-style with light 3D depth.